Oil prices could reach US$200/bbl in worst-case scenario as more than 11 million b/d of Gulf crude and condensate supply remains curtailed

LONDON/HOUSTON/SINGAPORE, May 20, 2026 (GLOBE NEWSWIRE) -- A prolonged closure of the Strait of Hormuz poses the single greatest threat to global energy markets in decades, according to a new Horizons report from Wood Mackenzie, Strait Talking: Iran War Scenarios and the Future of Energy. More than 11 million barrels per day (b/d) of Gulf crude and condensate production is currently curtailed. Meanwhile, over 80 million tonnes per annum (Mtpa) of LNG supply, equivalent to around 20% of global supply, remains inaccessible to global markets.

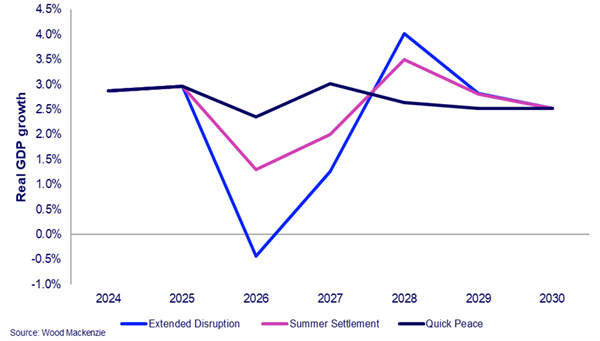

In its new report, Wood Mackenzie has shared three distinct scenarios: Quick Peace, Summer Settlement and Extended Disruption. Each scenario offers a different timeline for ending the conflict and reopening the Strait and assesses the potential impact on oil and gas supply, prices, energy demand and the broader global economy.

“The Strait of Hormuz is the most critical chokepoint in global energy markets, and a prolonged closure would become far more than an energy crisis,” said Peter Martin, head of economics at Wood Mackenzie. “The longer disruption persists, the greater the impact on energy prices, industrial activity, trade flows and global economic growth.”

Three paths forward, but risks are asymmetrical

Quick Peace

Under the most optimistic ‘Quick Peace’ scenario, a workable peace agreement is reached in the near term, and the Strait reopens by June. The global economy broadly returns to its pre-war trajectory by Q4 2026.

Crude prices fall sharply following a deal, with Dated Brent easing to around US$80/bbl by end-2026 and declining further to US$65/bbl in 2027 as the oil market returns to oversupply.

Global GDP growth slows from 3% in 2025 to 2.3% in 2026, with a recession limited to the Middle East. The global economy broadly returns to its pre-conflict trajectory by Q4 2026.

Summer Settlement

The ‘Summer Settlement’ scenario assumes the ceasefire holds but negotiations extend into late summer, with the Strait remaining largely closed until September.

Oil and LNG supply shortages persist through Q3 2026, driving a shallow global recession in H2 2026. Global GDP growth falls below 2% in 2026, resulting in modest yet permanent economic scarring compared to the pre-war baseline.

Extended Disruption

Under the most severe scenario, the Strait remains largely closed through the end of 2026, with recurring tensions triggering periods of renewed conflict and sustained supply disruption. Wood Mackenzie’s analysis indicates:

- Brent crude prices could approach US$200/bbl by end-2026, despite global oil demand falling by 6 million b/d year-on-year in H2 2026

- More than 11 million b/d of crude and condensate production remains shut in and global oil inventories continue to decline. Diesel and jet fuel prices could rise towards US$300/bbl in major refining centres by year end

- The global economy could contract by as much as 0.4% in 2026, marking the third global recession this century, with significant economic scarring

- Oil and gas importing countries could intensify efforts to reduce their import dependence by aggressively pursuing faster electrification

The regional economic impact would be severe and uneven. The Middle East could see GDP contract by 10.7% in 2026, while EU27 GDP declines by 1.5% in 2026 and 0.5% in 2027. US GDP growth would fall below 1% in both years, while China’s GDP growth slows to 3% in 2026.

“The long-term outlook points to structurally weaker oil prices than in our pre-conflict base case if importing countries accelerate efforts to reduce oil dependence,” said Alan Gelder, senior vice president for refining, chemicals & oil markets at Wood Mackenzie. “If electrification advances more aggressively and oil imports are displaced, this will add further downward pressure on prices, with Brent potentially trending US$10/bbl lower than the quick peace scenario in the medium/long-term. This outlook is, however, challenged by both the pace of the energy transition and higher energy costs for oil-importing economies that seek to reduce reliance on hydrocarbons.”

LNG market faces prolonged disruption and structural change

The report finds the global LNG market faces varying degrees of disruption under each of the three scenarios.

Even under Quick Peace, LNG markets remain tight through summer 2027 as Gulf export facilities recover gradually and construction delays slow the next wave of supply growth from the region.

A major global LNG expansion remains underway, with supply expected to increase by around 200 Mtpa by 2031, roughly 50% above current levels. The anticipated oversupply is delayed rather than eliminated.

Wood Mackenzie expects US LNG cargo cancellations may eventually be required to rebalance the market, with European TTF prices in the early 2030s almost half of 2026 levels of around US$14/mmbtu. Prices then stage a recovery through to 2035.

Under the Extended Disruption scenario, the market outlook becomes significantly more severe.

Some of the Gulf region’s existing 85 Mtpa of LNG supply could be permanently lost, while around 75 Mtpa of capacity currently under construction faces multi-year delays. As a result, global LNG supply could be on average 70 Mtpa lower than expected before the conflict.

“Persistent supply uncertainty would accelerate efforts to diversify away from imported LNG, supporting coal resilience and faster growth in renewables and electrification across Asia and Europe” said Massimo Di Odoardo, vice president of gas and LNG research at Wood Mackenzie. “LNG prices would remain elevated through to 2030 supporting investments in new LNG outside the Gulf, but lower long-term demand would risk undermining the industry’s future perspectives.”

A more fragmented global energy system

Beyond the immediate supply shock, Wood Mackenzie suggests that a prolonged conflict could accelerate structural changes across global energy markets.

Even after the Strait reopens, intermittent disruption could continue and reinforce the geopolitical risk attached to both oil and LNG trade flows, creating a more volatile pricing environment and increasing pressure on import-dependent economies to strengthen energy security.

In the Extended Disruption scenario, countries across Europe and Asia intensify efforts to reduce hydrocarbon dependence through accelerated electrification. At the same time, resource-rich producers outside the Gulf, including US LNG exporters, benefit from growing demand for supply diversification.

The report also highlights the increasing strategic importance of critical minerals supply chains as faster electrification and renewable deployment drive stronger demand for metals needed across clean energy technologies.

“The consequences of an extended disruption would extend well beyond energy markets,” Martin concluded. “It would test the resilience of global trade, industrial supply chains and economic growth simultaneously, reinforcing the urgency of achieving a resolution.”

About Wood Mackenzie:

Wood Mackenzie is the global leader in analytics, insights and proprietary data across the entire energy and natural resources landscape. For over 50 years our work has guided the decisions of the world’s most influential energy producers, utilities companies, financial institutions and governments. Now, with the world’s energy system more complex and interconnected than ever before, sector-specific views are no longer enough. That’s why we’ve redefined what’s possible with Intelligence Connected: the fusion of our unparalleled proprietary data with the sharpest analytical minds, all supercharged by Synoptic AI, to deliver a clear, interconnected view of the entire value chain. Our trusted team of 2,700 experts across 30 countries breaks siloes and connects industries, markets and regions across the globe to empower our customers to identify risk sooner, spot opportunity faster and make every decision with complete confidence. For more information, visit www.woodmac.com

Attachment

Hla Myat Mon Wood Mackenzie 85338860 hla.myatmon@woodmac.com

-

2026首届广东非遗品牌节圆满举办 非遗赋能乡村振兴 品牌点亮湾区文脉2026年5月18日,非遗赋能乡村振兴,品牌点亮湾区文脉——2026首届广东非遗品牌节·加一电光灯光秀非遗专场展演在广州加一光电文化基地圆满落幕。本次活动由中美2026-05-21

-

错过6 月再等一整年!Fac Tec China重磅打造汽车电子绿色智造实景展示区!展示、互动、论坛三管齐下,解锁汽车电子智能化、绿色化新模式2026年6月2日至4日,Fac Tec China 2026电子工厂设施展电子工厂设施展同期汽车电子专题展将在上海世博展览馆重磅推出“汽车电子绿色及智慧拆解实景展示区”。2026-05-21

-

凯德集团启动第二届“社区韧性资助计划”,提供400万新元支持亚洲弱势儿童与青少年2026年计划在四个市场,进一步拓展能力建设、跨领域合作及成果导向的资助模式 上海2026年5月21日 美通社 -- 2026年5月19日,凯德集团宣布正式启动第二届“社区韧性资2026-05-21

-

迈威生物宣布迈卫健®(地舒单抗注射液)增加适应症补充申请获批上海2026年5月21日 美通社 -- 迈威生物 (688062.SH,02493.HK),一家全产业链布局的创新型生物制药公司,宣布其全资子公司泰康生物自主研发的迈卫健® (地舒单抗注射液,研发2026-05-21

-

美国万通证券宣布为其客户Artificial Intelligence Technology Solutions Inc.(OTC:AITX)成功完成70万美元的私人配售纽约2026年5月21日 美通社 -- 美国万通证券作为美国金融业监管局及SIPC成员,提供全牌照服务的投资银行和证券经纪及交易商,于今日宣布已为其客户Artificial Intellig2026-05-21

-

AMD股价暴跌17%创近9年之最,苏姿丰紧急回应:AI增速远超想象

-

Ledger 中国销售渠道说明:广州馨潇贸易有限公司官方直营渠道公示

-

江苏省脑机接口产业联盟在宁成立,麦澜德分享前沿成果

-

艾芬达入选国家知识产权强国建设示范创建对象:二十载长期主义,兑现每一份用户价值

-

Esentia宣布成功完成2033年到期的6.125%优先票据和2038年到期的6.500%优先票据的定价

-

中荷人寿北京分公司成功举办中荷创享家品牌发布暨协同发展启航仪式

-

慧启赣疆 聚势共赢丨慧友酒店集团江西品鉴会书写区域文旅融合新篇

-

电影《一秒》定档:2026年,活在这一秒

-

西藏斜视患儿寒假进京手术成功,千里护航点亮视觉未来

-

年度盛典|卓兴半导体2025年度总结表彰暨 2026 年迎新晚会